Falling behind on mortgage payments is an incredibly stressful experience, and the looming threat of foreclosure can feel overwhelming. When you’re facing this difficult situation, it’s easy to feel lost, confused, and unsure of where to turn for help. But before you lose hope, it’s important to know that you have options. For many Florida homeowners, understanding what is a short sale in real estate is the first step toward finding a viable alternative that can help you avoid foreclosure and move forward with your life.

We’re here to guide you through this complex process with clarity and support. In this comprehensive guide, we will simplify the concept of a short sale and explain exactly what it means for you as a homeowner in Florida. We’ll walk you through how the process works, discuss the potential impact on your credit, and provide the straightforward information you need to determine if a short sale is the right choice to protect your financial future. You don’t have to navigate this journey alone.

Key Takeaways

- Gain a clear understanding of what is a short sale in real estate and why it’s a potential solution when your mortgage is “underwater.”

- Discover the typical step-by-step process for a short sale in Florida and why patience and expert guidance are essential for success.

- Learn the critical differences between a short sale and a foreclosure to help you make a proactive, informed decision about your future.

- Understand the key requirements lenders look for and the first steps you need to take to determine if you can qualify for a short sale.

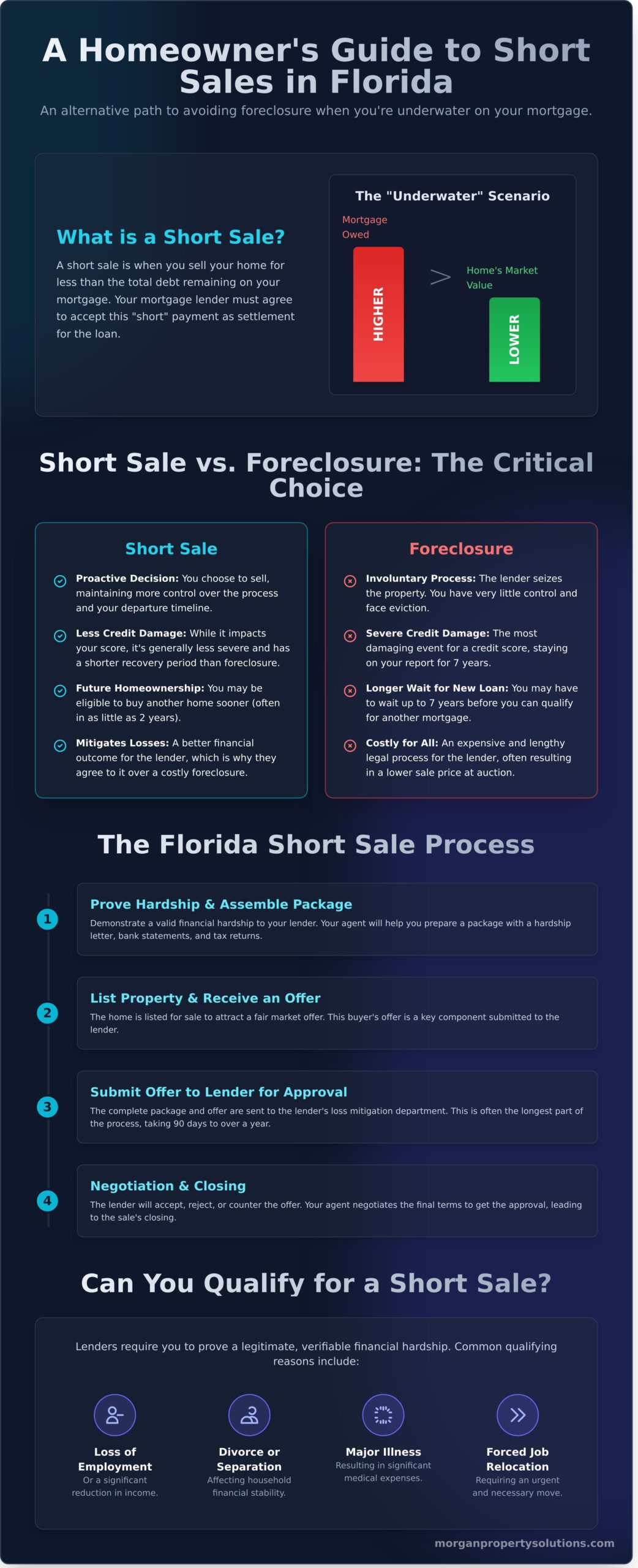

What is a Short Sale? A Simple Definition for Homeowners

Facing financial hardship can be incredibly stressful, and navigating the complexities of real estate at the same time can feel overwhelming. If you’re struggling to make mortgage payments, it’s important to know your options. Understanding what is a short sale in real estate is the first step toward finding a viable solution that can help you avoid foreclosure and move forward.

Simply put, a short sale occurs when a homeowner sells their property for a price that is less than the outstanding balance on their mortgage. This typically happens when a homeowner is “underwater” or “upside-down” on their loan, meaning the current market value of their home is lower than what they still owe. For the sale to proceed, the mortgage lender must agree to accept a “short” payoff and release the lien on the property. To provide a basic overview, Wikipedia’s answer to what is a short sale? confirms it is a sale where the proceeds fall short of the debt.

A successful short sale involves several key players, each with a critical role:

- The Seller: The homeowner who needs to sell due to a documented financial hardship.

- The Lender: The bank or financial institution that holds the mortgage and must approve the sale.

- The Buyer: An individual or entity making an offer to purchase the property.

- The Real Estate Agent: An experienced professional who guides the seller and negotiates with the lender.

Why Would a Bank Agree to a Short Sale?

It may seem counterintuitive for a lender to willingly accept a loss, but a short sale is often a sound business decision for them. The foreclosure process can be extremely costly and time-consuming for a bank, involving legal fees, property maintenance, and the uncertainty of an auction. A short sale allows them to mitigate those losses, recover a significant portion of the loan amount quickly, and avoid the burden of owning and managing real estate.

The Difference Between a Short Sale and a Traditional Sale

The key difference lies in equity and control. In a traditional sale, the homeowner has equity, meaning the home is worth more than the loan. The seller controls the transaction and keeps the profit after the mortgage is paid off. In a short sale, however, the lender must approve the final sale price and all terms. Because of the extra layer of bank approval, the timeline for a short sale is typically much longer and more unpredictable than a traditional sale.

The Florida Short Sale Process: A Step-by-Step Walkthrough

Navigating a short sale in Florida requires patience, persistence, and the right professional guide. While understanding what is a short sale in real estate is the first step, knowing the process is what brings peace of mind. The timeline can often take anywhere from 90 days to over a year, but with an experienced agent managing the details, it becomes a clear path to a fresh start. A key point of relief for many homeowners is that in a short sale, the lender pays the real estate commissions, not you.

We’re here to make this complex process simple. Here is a clear, step-by-step guide to what you can expect.

Step 1: Proving Hardship and Assembling Your Package

The first step is to demonstrate to your lender that you have a legitimate financial hardship preventing you from making mortgage payments. This isn’t just about being “underwater.” Valid hardships include:

- Loss of employment or reduced income

- Divorce or separation

- Major illness and medical expenses

- Job relocation

Your agent will help you assemble a “short sale package,” which includes a formal hardship letter, recent bank statements, pay stubs, and tax returns. This package provides the lender with a complete financial picture and justifies your request.

Step 2: Listing the Property and Receiving an Offer

Pricing a short sale property is a strategic decision. The goal is to attract a fair market offer quickly to present to the lender for consideration. Your real estate agent will market the home clearly as a short sale, ensuring potential buyers understand that any offer is contingent on lender approval. Once a buyer submits an offer, it becomes the cornerstone of the package sent to your bank.

Step 3: Submitting the Offer to the Lender for Approval

With a buyer’s offer in hand, your agent submits the complete package to the lender’s loss mitigation department. The bank will then order its own property valuation, typically a Broker Price Opinion (BPO), to determine the home’s current market value. This stage, where the bank evaluates the offer, is often the most time-consuming part of the entire Florida Short Sale Process. Consistent follow-up from your agent is critical here.

Step 4: Negotiation and Closing

After its review, the lender will respond to the offer. They can accept it, reject it, or issue a counteroffer. This is where an experienced negotiator is invaluable. Your agent will work directly with the bank to secure an approval that is favorable to you, including the forgiveness of any remaining mortgage debt. Once the lender provides written approval, the transaction proceeds to closing much like a traditional sale.

Short Sale vs. Foreclosure in Florida: Which is Better?

Facing the potential loss of your home is incredibly stressful, and the decision between a short sale and foreclosure is one of the most critical you’ll make. The fundamental difference is about control. A short sale is a proactive step you take to resolve your mortgage debt, while a foreclosure is a reactive legal process initiated by your lender against you. While both have serious financial consequences, a short sale allows you to manage the outcome and often leads to a better long-term recovery.

Impact on Your Credit Score

Both a short sale and a foreclosure will negatively impact your credit score, but not equally. A foreclosure is one of the most damaging events that can appear on a credit report, often causing a score to drop by 150 points or more. A short sale is also damaging but is typically viewed more favorably by credit scoring models. It is often reported as “settled for less than the full amount,” which, while not ideal, is less severe than a foreclosure judgment.

Future Home Buying Eligibility

Regaining the ability to purchase a home is a major goal for many facing this situation. The path back to homeownership is generally much shorter after a short sale. Here’s a typical comparison:

- After a Short Sale: You may be eligible for a new FHA or conventional mortgage in as little as 2 to 4 years, depending on the circumstances.

- After a Foreclosure: The waiting period is significantly longer, often lasting from 5 to 7 years.

Lenders often view a short sale as an act of taking responsibility, which can work in your favor when you’re ready to apply for a new loan. If you’re already thinking ahead to your next purchase, our Orlando real estate guide can help you understand the local market and neighborhoods as you plan your fresh start.

The Deficiency Judgment Factor in Florida

This is where understanding what is a short sale in real estate becomes crucial for Floridians. Florida is a “recourse” state, which means if your home sells for less than the total mortgage balance, the lender can legally pursue you for the difference. This leftover debt is called a deficiency judgment. Understanding the core differences in the Short Sale vs. Foreclosure options is vital because a lender can seek this judgment after either event. However, a key advantage of a short sale is the opportunity to negotiate a deficiency waiver. A skilled real estate professional will make this a primary goal, working to get the lender to agree in writing to forgive the remaining debt, providing you with a truly fresh start.

Navigating these complex financial and legal waters requires an experienced guide. If you’re exploring your options in Florida, the team at morganpropertysolutions.com is here to provide the clear, professional support you need to make the best decision for your future.

Preparing for a Short Sale: How to Qualify and Get Started

Facing a potential short sale can feel overwhelming, but taking proactive, informed steps is the key to navigating the process successfully. The first and most important step is to accept the situation and seek expert help. While you now understand what is a short sale in real estate, preparing for one requires a clear, strategic approach. Remember, not everyone will qualify, as the lender has the final say. Being organized with your finances and responsive to requests is absolutely crucial for reaching a positive outcome. We recommend gathering all your financial documents as early as possible to get a head start.

Do You Qualify? Key Requirements

Your lender will need to be convinced that a short sale is their best option. To approve your request, they will typically require you to meet three core conditions:

- You are ‘underwater’ on your mortgage. This means you owe more on your home loan than the property’s current fair market value. An appraisal or a Broker Price Opinion (BPO) will be used to determine this.

- You have a valid financial hardship. You must be able to document a significant, non-temporary life event that prevents you from making mortgage payments. Common examples include job loss, divorce, major medical bills, or a forced relocation.

- You have insufficient assets. The lender will review your bank statements, savings, and other assets. If you have significant funds available to pay the mortgage shortfall, your application will likely be denied.

Finding the Right Real Estate Agent

You should not attempt to navigate a short sale alone. Your most important ally in this process is a real estate agent with specific, verifiable short sale experience. They will manage communication with the lender, market the property, and guide you through the complex paperwork. When interviewing agents, look for those with credentials like the Short Sales and Foreclosure Resource (SFR®) certification. Ask about their success rate and their experience with major Florida lenders. Find a trusted real estate partner to guide you through every step with confidence and care.

To see an example of how a professional real estate team provides in-depth community information for those looking to start fresh in a new area, you can find out more.

Common Mistakes to Avoid

A successful short sale depends on avoiding common pitfalls that can derail the process. Be mindful to steer clear of these errors:

- Waiting too long to take action. Time is critical. The sooner you start, the more control you have. Waiting until foreclosure proceedings are imminent severely limits your options.

- Not being truthful about your situation. Be completely transparent in your hardship letter and financial statements. Lenders will verify everything, and any dishonesty will lead to an immediate denial.

- Navigating the process without an expert. The extensive paperwork, strict deadlines, and constant negotiation with the bank require specialized knowledge. An experienced agent is essential.

For more guidance on selling your property, explore our real estate articles for more seller tips.

Your Path Forward: Making Sense of Your Florida Short Sale

Ultimately, understanding what is a short sale in real estate is the first step toward regaining control of your financial future. This process, while complex, allows you to sell your home for less than you owe and often presents a more favorable alternative to foreclosure for Florida homeowners. Knowing the steps and qualification requirements gives you the power to make an informed decision, but you don’t have to navigate it alone.

Facing a tough situation can be incredibly stressful, but expert guidance can make all the difference. At Morgan Property Solutions Inc., we specialize in making complex real estate simple for homeowners just like you. With over 20 years of combined experience and an A+ rating from the Better Business Bureau, our team is here to help you understand your options with clarity and compassion. Facing a tough situation? Let’s discuss your options. Talk to our Central Florida real estate experts today.

Remember, a difficult circumstance doesn’t have to define your future. There is a path forward, and we’re here to help you find it.

For many, that path involves learning new financial strategies to build lasting wealth. Educational resources from firms like Property-CEO are designed to teach the fundamentals of property investment, helping individuals create a more secure financial future.

Frequently Asked Questions About Florida Short Sales

How long does a short sale take in Florida?

In Florida, a short sale typically takes anywhere from four to six months, though some complex cases can take longer. The timeline depends heavily on the lender’s efficiency, the number of liens on the property, and how quickly an offer is received. The process involves extensive paperwork and negotiation between all parties. Having an experienced agent to manage this process is crucial to keep things moving forward as smoothly and predictably as possible, providing you with peace of mind.

Do I have to pay taxes on the forgiven debt in a short sale?

This is a common and important concern. While past legislation often protected homeowners from paying taxes on forgiven mortgage debt, tax laws can and do change. It is absolutely essential to consult with a qualified tax advisor or CPA to understand your specific situation and potential tax liability. They can provide the most current information and guide you on how to handle any forgiven debt, ensuring there are no financial surprises after the sale is complete.

Can I stay in my home during the short sale process?

Yes, you can and should remain in your home throughout the short sale process. You are still the legal owner of the property until the sale officially closes and the title is transferred to the new buyer. It is important to continue maintaining the home and to cooperate with your real estate agent to allow for showings to potential buyers. This helps ensure the process moves forward efficiently and leads to a successful outcome for everyone involved.

Does it cost me anything to do a short sale?

In nearly all short sale situations, the seller pays nothing out of pocket. The real estate commissions, closing costs, and other associated fees are paid from the sale proceeds at closing. These costs are all presented to your lender for approval as part of the short sale package. Our goal is to make this process as simple and stress-free as possible, and that includes ensuring you are not burdened with the typical costs associated with selling a home.

What is a ‘deficiency waiver’ and why is it important?

When you ask what is a short sale in real estate, understanding the deficiency is key. The “deficiency” is the difference between what you owe on your mortgage and the lower price the home sells for. A ‘deficiency waiver’ is a legally binding agreement from your lender stating they will not pursue you for this amount after the sale. Securing this waiver is one of our most important goals, as it provides you with a true fresh start without lingering debt.

Will a short sale stop a foreclosure auction?

A short sale can often stop a foreclosure auction, but it is not automatic and requires swift action. Once a complete short sale package and a valid purchase offer are submitted, we can formally request that the lender postpone the scheduled auction date. Most lenders prefer a short sale to a foreclosure and will cooperate, but time is critical. If you are facing foreclosure, starting the process immediately gives you the best possible chance of a successful resolution.

Article by

Oliver Overton-Morgan

Oliver Overton-Morgan is a full-time Real Estate Broker since 2003, with years of experience helping thousands of people purchase and sell real estate throughout Central Florida. He holds a Graduate Realtor Institute designation, LCAM, and has held licenses in good standing as a Florida Mortgage Broker and a Notary Public. Oliver immigrated to central Florida in 2001, and within 5 years Oliver built a successful Real Estate brokerage in central Florida, where he recruited over 75 Sales Associates with 25+ million in sales production.