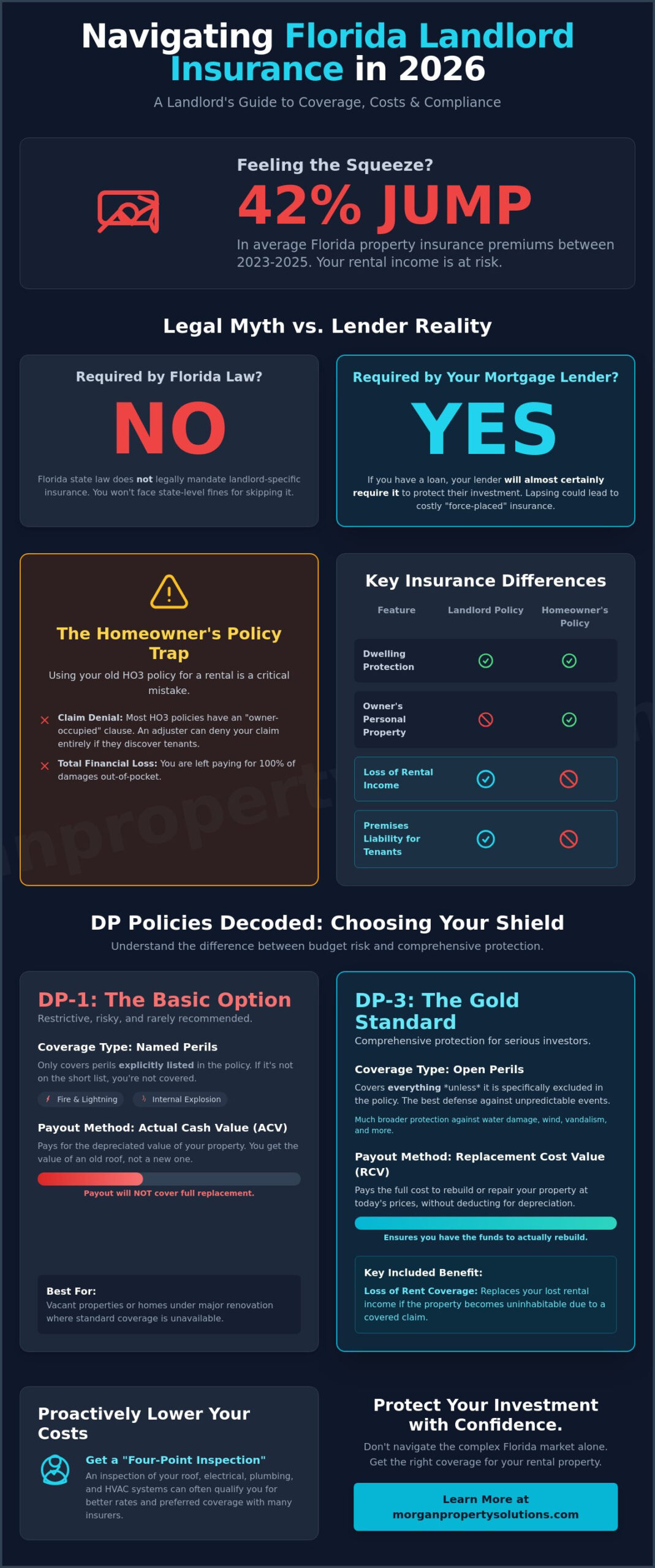

With Florida property insurance premiums jumping by an average of 42% between 2023 and 2025, you might feel like your rental income is being swallowed whole by monthly bills. It’s frustrating to watch your profits shrink while you’re left wondering if you’re even covered for the next big storm. You probably feel the pressure of trying to balance “good enough” coverage with a price tag that doesn’t break the bank. Understanding the specific landlord insurance florida requirements is the first step toward regaining control of your investment.

We’re here to help you make sense of these rules so you can protect your property with total confidence. You’ll get a clear, human-friendly guide to exactly what you need in 2026 without the usual industry jargon. Our goal is to make this process simple and stress-free for you. You can trust us to guide you through the complexities of the current Florida market every step of the way.

In this guide, we will break down the differences between DP-1 and DP-3 policies, explain what the law actually requires versus what lenders demand, and share proven ways to lower your costs.

Key Takeaways

- While Florida law is surprisingly quiet on the matter, we’ll explain why your mortgage lender and your own financial safety definitely won’t be.

- Get a clear look at the DP policy hierarchy so you can choose a plan that fits your budget without leaving your assets exposed.

- Understand the specific landlord insurance florida requirements regarding hurricane deductibles and the common mistakes owners make when it comes to flood protection.

- Learn how simple steps like a “Four-Point Inspection” can help you qualify for better rates and keep your 2026 insurance costs under control.

Do You Actually Need Landlord Insurance in Florida? Legal vs. Practical Realities

If you are looking for a simple “yes” or “no” regarding Florida state law, the answer is no. Florida does not legally mandate that property owners carry a specific landlord policy. You won’t face state-level fines or lose your business license just for skipping it. However, this technicality is often a trap for new investors. While the state stays out of it, your mortgage lender definitely won’t. If you have a loan on your property, your contract almost certainly requires you to maintain adequate coverage that protects their investment.

In 2026, the stakes are higher than ever for property owners in Central Florida. Between rising repair costs and the unpredictable nature of tropical weather, “going bare” or staying uninsured is a massive gamble. Many owners fall into the “Homeowners Policy Trap” by keeping their standard HO3 policy active after moving out and bringing in tenants. This is a dangerous mistake. Most standard policies include an “owner-occupied” clause. If a pipe bursts or a fire occurs and the adjuster discovers the home is a rental, they can deny your claim entirely. You are then left paying for 100% of the damages out of pocket.

Understanding the specific Landlords’ insurance nuances is the first step to protecting your asset. At Morgan Property Solutions, we focus on making these transitions simple. You can find more guidance on managing these risks in our landlord resources section.

Lender Requirements and the “Force-Placed” Risk

Lenders view rental properties as higher risk than primary residences. Because of this, they monitor your insurance status closely. If your lender discovers you don’t meet the landlord insurance florida requirements outlined in your mortgage, they will purchase “force-placed” insurance for you. This is never a win for the landlord. Force-placed policies often cost 200% to 300% more than a policy you would find on your own. To make matters worse, these expensive policies usually only protect the lender’s interest in the structure, leaving your liability and personal property completely exposed.

Landlord vs. Homeowners Insurance: The Core Differences

The differences between these two types of coverage are functional and financial. While a homeowners policy covers your personal belongings like furniture and clothes, a landlord policy focuses on the dwelling itself. It also provides two things a standard policy won’t:

- Loss of Rental Income: If a fire makes the home uninhabitable, this coverage pays you the rent you lose while the home is being repaired.

- Premises Liability: This protects you if a tenant or guest is injured on the property and decides to sue.

In the 2026 market, having a policy that accounts for these specific rental risks isn’t just a suggestion; it’s a fundamental part of a professional investment strategy.

Understanding the Three Tiers: DP-1, DP-2, and DP-3 Policies

Choosing the right coverage means looking closely at the Dwelling Fire (DP) hierarchy. In Florida, these tiers determine exactly what events are covered and how you’re paid after a loss. It’s a balance between your monthly budget and your long-term financial safety. While most landlord insurance florida requirements aren’t set by state law, your mortgage lender will usually require a specific level of protection to secure their investment; to find a plan that satisfies these requirements, you can learn more about SI Insurance.

The main difference between these tiers involves “Named Perils” versus “Open Perils.” A named peril policy only covers the specific items listed in the document. If it isn’t on the list, you’re on your own. An open peril policy covers everything except for a few specific exclusions. For a landlord in a high-risk state like Florida, this distinction is the difference between a minor setback and a total financial loss.

DP-1: The Basic (and Risky) Budget Option

A DP-1 policy is the most restrictive form of coverage available. It only protects against a very short list of named perils, which usually includes just fire, lightning, and internal explosions. If a pipe bursts or a vandal tags your building, you’re likely paying for the repairs out of pocket. These policies pay out based on Actual Cash Value (ACV). This means the insurance company subtracts depreciation from your payout. If your 12-year-old roof is destroyed, you won’t get enough to buy a new one; you’ll get the value of an old, used roof. This policy is mostly for vacant properties or homes undergoing heavy renovation where standard coverage isn’t an option.

DP-3: The Gold Standard for Florida Landlords

For most rental properties, a DP-3 policy is the smart choice. It uses “Open Peril” coverage for the structure. This means every type of damage is covered unless the policy specifically lists it as an exclusion. It’s the best defense against the unpredictable Florida weather. Most importantly, DP-3 policies typically provide Replacement Cost Value (RCV). This ensures you can actually rebuild the home at today’s construction prices without worrying about depreciation. You also get “Loss of Rent” coverage. If a fire makes the home uninhabitable, the insurance company replaces your rental income while repairs happen. This keeps your cash flow steady even when the property is empty.

When you’re trying to find the right balance for your rental, consider these differences:

- DP-1: Best for short-term vacancies or “as-is” investment flips.

- DP-2: A middle ground that names about 16 specific perils like falling objects or the weight of ice.

- DP-3: Essential for long-term rentals and high-value assets where you want total peace of mind.

Investing in a DP-3 policy might cost more in annual premiums, but it prevents a single bad storm from wiping out your profits. We’ve seen owners save a few dollars on premiums only to lose thousands because their policy didn’t cover water damage or theft. Making real estate simple means making sure you’re protected before the first tenant moves in.

Navigating Florida’s Unique Risks: Hurricanes, Floods, and Liability

Florida offers incredible opportunities for rental income, but our environment demands a specific approach to protection. Meeting the basic landlord insurance florida requirements is just the starting point. You also need to account for the tropical climate and legal landscape that define the Sunshine State. We’re here to help you understand these complexities so you can protect your investment with confidence.

Hurricane Deductibles and Windstorm Coverage

One of the biggest surprises for new owners is the hurricane deductible. This isn’t a flat dollar amount like your standard $500 or $1,000 deductible for a fire or a theft. Instead, it’s a percentage of your property’s total insured value, typically ranging from 2%, 5%, or even 10%. If your rental is insured for $400,000 and you have a 5% deductible, you’ll pay $20,000 out of pocket before your coverage kicks in for storm damage.

The Florida Calendar Year Hurricane Deductible rule ensures that policyholders only pay their hurricane deductible once per calendar year regardless of how many named storms impact the property. If you’re managing property in high-risk coastal zones like Tampa or Miami, you might need to secure a separate windstorm policy if your primary carrier excludes wind and hail. We always recommend checking your policy declarations page to confirm wind coverage is active, as some “surplus lines” carriers in Florida may exclude it by default.

The Flood Insurance Gap

A common mistake is assuming that landlord insurance covers flooding. It doesn’t. Standard policies cover “sudden and accidental” water damage, like a burst pipe, but they won’t cover rising water from a storm surge or heavy rain. You’ll need a separate policy through the National Flood Insurance Program (NFIP) or a private carrier to be fully protected.

- Check your zone: Use the FEMA Map Service Center to look up properties in Orlando or Lake Nona to see if you’re in a high-risk Special Flood Hazard Area.

- Inland risks: Don’t assume you’re safe just because you’re inland; 25% of all flood insurance claims come from moderate-to-low risk areas.

- Private vs. NFIP: Private flood insurance often offers higher limits for loss of use, which pays your lost rental income while the home is being repaired.

Our team at Morgan Property Solutions focuses on making real estate simple, and that includes helping you identify these “invisible” gaps before they become expensive problems.

Liability and Mold Riders

Liability protection is your most important shield against legal trouble. If a tenant trips on a loose floorboard or a guest is injured by a falling branch, you’re the one held responsible. We suggest a minimum of $300,000 in liability coverage, though $500,000 is safer for most Florida landlords. This coverage pays for legal defense fees and settlements, which can easily bankrupt an unprotected owner.

Finally, you must address mold and fungus. Central Florida’s 74% average humidity makes mold growth a constant threat, especially after a minor leak. Most standard policies limit mold remediation to $10,000, which barely covers the basics. Adding a specific “Mold and Fungus” rider ensures you have the funds to properly treat the property and keep your tenants safe. You can find more guidance on maintaining a safe rental environment in our landlord resources section.

How to Lower Your Florida Landlord Insurance Premiums in 2026

Florida insurance costs have climbed significantly over the last few years, but you aren’t powerless against rising rates. While meeting landlord insurance florida requirements is a non-negotiable part of protecting your investment, there are several ways to make your property more attractive to private carriers. Most insurers in 2026 are looking for “hardened” properties that can withstand the unique pressures of our tropical climate. By taking proactive steps, you can move your property out of high-risk categories and into more affordable tiers.

The Four-Point Inspection is the most influential document for your yearly rates. This report covers your roof, electrical system, plumbing, and HVAC. If your roof is older than 15 years or your electrical panel is an outdated brand like Federal Pacific, private insurers might deny coverage entirely. Keeping these systems updated isn’t just about maintenance; it’s the primary way to avoid being forced into Citizens Property Insurance. Citizens is the state-backed “insurer of last resort,” and while it provides a safety net, the goal for most landlords in 2026 is to find coverage in the private market where policies are often more comprehensive.

Your choice of tenant also plays an indirect role in your long-term costs. High tenant turnover often leads to more frequent “wear and tear” issues that can spiral into liability claims. We’ve found that stable, long-term tenants who treat the home as their own are less likely to ignore a small leak that could turn into a massive mold claim. Consistent screening and professional management help keep these risks low.

Property Upgrades That Pay for Themselves

Wind mitigation is your best friend when it comes to discounts. A formal wind mitigation inspection usually costs between $75 and $150, but it can save you 25% or more on your premium. Insurers look for roof-to-wall attachments like hurricane straps and impact-resistant windows. Even if you don’t replace every window, adding Florida-rated shutters can trigger significant credits. Updating the “Big Four” systems is equally vital. Replacing old polybutylene pipes or a 20-year-old water heater removes the “hidden” risks that carriers hate. You can also snag a “Smart Home” discount by installing simple leak sensors under sinks and near the water heater. These devices alert you to moisture before a pipe burst ruins the flooring.

Policy Tweaks and Bundling Strategies

Adjusting your policy structure is a quick way to find relief. Increasing your deductible from $1,000 to $2,500 or $5,000 can lower your monthly payments by 10% to 15%. Just make sure you keep that deductible amount in a dedicated reserve fund so you aren’t caught off guard. Bundling your landlord policy with your primary residence or auto insurance is another easy win, often resulting in a multi-policy discount of around 5%. One of the smartest moves you can make is to require tenants to carry renters insurance. This protects their personal belongings and provides them with liability coverage, which prevents small accidents from hitting your own policy first.

Simplifying Your Protection: How Property Management Mitigates Risk

Meeting the basic landlord insurance florida requirements is a vital step for any investor, but it’s really only half of the equation. Think of insurance as your safety net and risk mitigation as the floor you’re standing on. You don’t want to test that net unless it’s absolutely necessary. When you focus on active risk management, you keep your investment out of the “claim zone,” which helps maintain your property value and keeps your long-term premiums from skyrocketing. Professional property management in Orlando acts as your first line of defense against the most common reasons for insurance claims.

Our team at Morgan Property Solutions understands that a proactive approach is always more affordable than a reactive one. By implementing systems that address liability and physical damage before they escalate, we protect your bottom line. We’ve spent over 20 years helping owners navigate the complexities of the Florida market, and we know exactly where the pitfalls are. It’s about more than just collecting rent; it’s about creating a secure environment where your assets can grow without unnecessary legal or financial interruptions.

The Power of Professional Tenant Screening

A “high-risk” tenant can cause more financial damage in a single month than a tropical storm. This is why we stick to rigorous screening criteria to stop problems before they ever sign a lease. We look at credit history, criminal records, and previous rental performance to ensure we’re placing reliable individuals in your home. This process significantly reduces the likelihood of tenant-caused damage or messy liability lawsuits that could trigger your insurance policy.

Animals are another common source of insurance anxiety. Since roughly 66 percent of American households include a pet, you can’t simply ignore this segment of the market. We use our Petscreening.com partnership to vet every animal. This service verifies vaccinations, behavior history, and assistance animal documentation. It gives you an extra layer of protection against bite liabilities and property destruction, ensuring you stay compliant with all landlord insurance florida requirements regarding animal coverage.

Regular Inspections and Preventative Maintenance

Insurance adjusters love documentation. If you ever have to file a claim for a major leak or structural issue, having a clear paper trail of regular inspections is invaluable. We perform routine walk-throughs to catch small issues like a dripping water heater or a loose roof shingle. Catching a small leak today prevents a $15,000 black mold remediation project next year. Most insurance policies won’t cover damage caused by “slow leaks” or lack of maintenance, so our eyes on the ground protect your coverage status.

We handle the maintenance coordination and the technical details, often working with trusted local specialists like Alberto Pro Plumbing to keep your systems in peak condition, so you don’t have to. Our goal is to make your experience as a landlord completely stress-free. By managing the day-to-day risks, we ensure you can enjoy the profits of your investment while we take care of the heavy lifting. You can trust us to guide you through every step of the process, making real estate simple and secure.

Secure Your Investment and Start Stress-Free Management

Protecting your rental property in 2026 shouldn’t feel like a guessing game. You’ve learned that while Florida law doesn’t strictly mandate coverage, meeting landlord insurance florida requirements is essential for satisfying mortgage lenders and protecting your personal wealth. Whether you choose a basic DP-1 or a more comprehensive DP-3 policy, the right choice depends on your specific risk level and the age of your property. Managing high-stakes risks like hurricane damage and liability claims is much easier when you have a solid plan in place.

Our team brings over 20 years of Central Florida expertise to the table, and our A+ BBB Rating shows how much we care about our clients. We specialize in comprehensive risk-mitigation, ensuring that professional management handles the heavy lifting so you don’t have to. We’re ready to help you navigate the complexities of the local market with confidence and ease.

Let us simplify your rental journey; contact Morgan Property Solutions today!

We look forward to helping you succeed and making your real estate experience as smooth as possible.

Frequently Asked Questions

Is landlord insurance legally required by the state of Florida?

Florida state law doesn’t legally mandate landlord insurance for property owners. However, if you have a mortgage through a lender like Wells Fargo or Chase, they’ll almost certainly require a policy to protect their investment. Even without a loan, skipping this coverage is risky because standard homeowners policies often deny claims if they find out the property is a full-time rental.

How much does landlord insurance typically cost in Orlando vs. Miami?

Costs vary significantly based on your ZIP code and the home’s age. In Orlando, landlords might see annual premiums around $2,500, while Miami owners often pay $4,000 or more due to increased windstorm risks. These rates reflect the 2024 market trends where South Florida premiums sit about 60% higher than inland cities. Understanding these landlord insurance florida requirements helps you budget accurately for your investment property.

Does landlord insurance cover tenant-caused damage to the property?

Most policies cover sudden and accidental damage caused by a tenant, like a kitchen fire or a major water overflow. They won’t pay for wear and tear, such as stained carpets or scuffed walls. If a tenant intentionally trashes the place, you’ll need to check if your specific policy includes vandalism coverage, as some basic plans exclude it to keep costs down.

What is the difference between a DP-1 and a DP-3 policy?

A DP-1 policy is a basic, named peril plan that only covers specific events like fire or lightning. It usually pays out actual cash value, which factors in depreciation. A DP-3 policy is the gold standard for landlord insurance florida requirements because it’s an open peril plan. It covers everything unless specifically excluded and typically pays the full replacement cost, making it much safer for your investment.

Can I just keep my homeowners insurance if I rent out my Florida home?

You shouldn’t rely on a standard homeowners policy once you move out and let tenants move in. Most insurance carriers will deny a claim if they discover the home is no longer your primary residence. Switching to a dedicated landlord policy ensures you have liability protection and coverage for loss of rent if a disaster makes the home uninhabitable for your tenants.

Do I need a separate flood insurance policy for my rental property?

You definitely need a separate flood policy because standard landlord insurance doesn’t cover rising ground water. With 40% of Florida’s population living in high-risk flood zones according to FEMA, this is a critical add-on. Whether you use the National Flood Insurance Program or a private carrier, it’s the only way to protect your building from storm surges or heavy tropical rains.

How does a hurricane deductible work for Florida landlords?

Hurricane deductibles in Florida work as a percentage of your total dwelling coverage rather than a flat dollar amount. If your rental is insured for $300,000 and you have a 5% hurricane deductible, you’ll pay $15,000 out of pocket before the insurance kicks in. This trigger usually applies once the National Weather Service declares a hurricane watch or warning for any part of Florida.

Should I require my tenants to have renters insurance?

We always recommend requiring tenants to carry their own renters insurance policy. It protects their personal belongings and, more importantly, provides them with personal liability coverage. If a tenant accidentally starts a fire, their insurance can cover the damages and their temporary housing. This keeps the claims off your own policy, which helps keep your long-term premiums from spiking after a minor accident.

Article by

Oliver Overton-Morgan

Oliver Overton-Morgan is a full-time Real Estate Broker since 2003, with years of experience helping thousands of people purchase and sell real estate throughout Central Florida. He holds a Graduate Realtor Institute designation, LCAM, and has held licenses in good standing as a Florida Mortgage Broker and a Notary Public. Oliver immigrated to central Florida in 2001, and within 5 years Oliver built a successful Real Estate brokerage in central Florida, where he recruited over 75 Sales Associates with 25+ million in sales production.