Did you know that the average Florida homeowner is now looking at insurance premiums that are nearly triple the national average? It’s a startling figure that can make anyone hesitate. If you’re feeling a bit overwhelmed by the fast-paced competition in areas like Lake Nona or the complex math of modern mortgage rates, you’re certainly not alone. Many people worry that the dream of owning a home is slipping away. However, mastering the steps to buying a house in florida for the first time is still very much possible with the right strategy in place.

We agree that the process feels more complicated than it used to be. That’s why we created this plain-English guide to help you move from fixing your credit to snagging your first set of keys. We promise to give you a clear roadmap that covers everything from Florida-specific tax benefits to choosing a dependable local agent. You’ll get a full preview of what to expect in 2026, including how to handle high insurance costs and which down payment assistance programs are actually worth your time. Let’s turn that anxiety into a solid plan for your future.

Key Takeaways

- Learn why your credit score is the ultimate gatekeeper and how to refine your debt-to-income ratio before you ever step foot in a bank.

- We break down the essential steps to buying a house in florida for the first time, helping you navigate everything from fast-paced neighborhood growth to local commute times.

- Understand the “Florida Factor” and why details like the age of a roof can make or break your ability to find a reasonable insurance policy.

- Discover how to protect your money using escrow and create a winning offer that captures a seller’s attention without stretching your budget too thin.

- Find out how to claim your first big financial win after closing by using state-specific tax exemptions and property assessment caps.

Getting Your Finances Florida-Ready for 2026

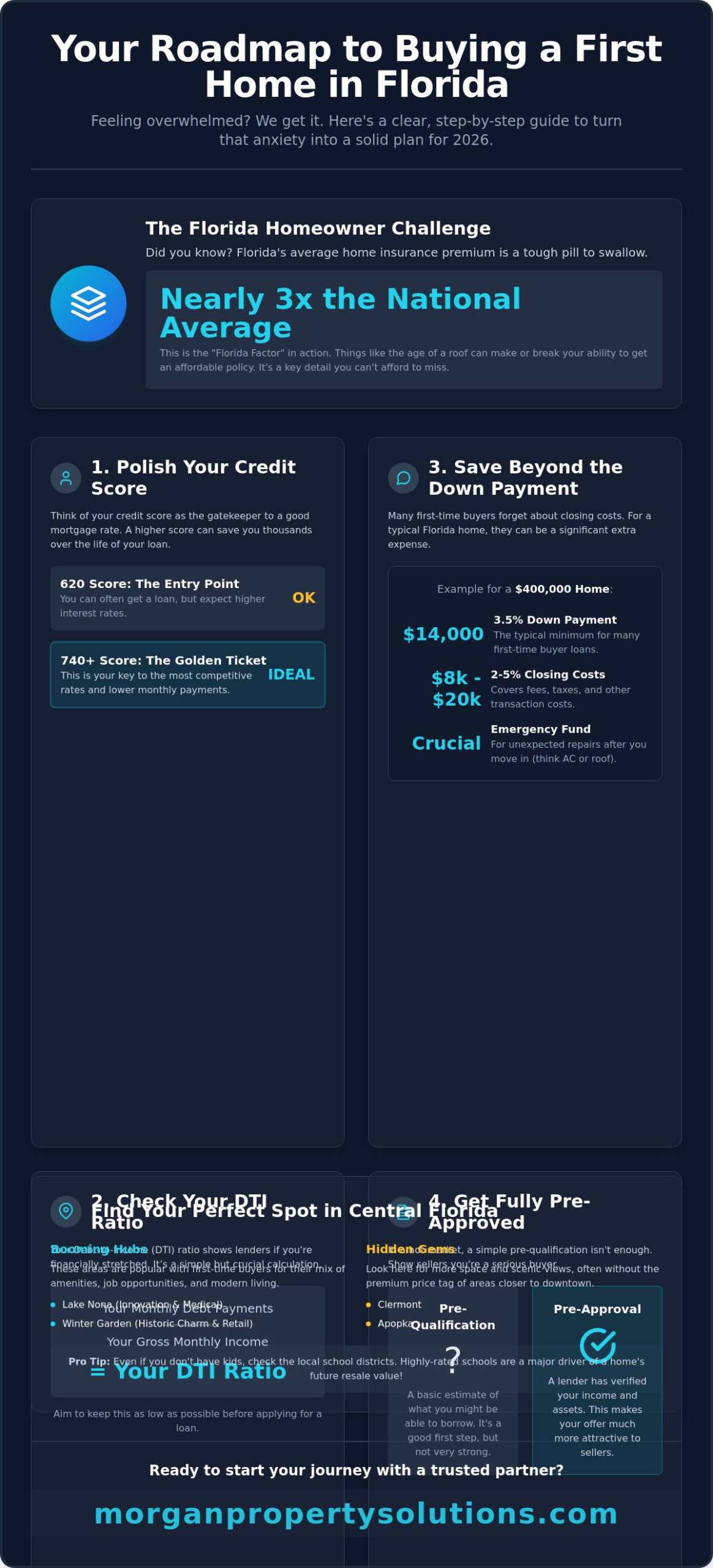

Before you start scrolling through online listings, you need to look at your bank account through the eyes of a lender. In 2026, the Florida market requires a bit more financial muscle than it did just a few years ago. One of the most critical steps to buying a house in florida for the first time is ensuring your financial foundation is rock solid before you ever talk to an agent. Lenders are looking for stability. They want to see that you can comfortably handle monthly payments alongside Florida’s unique costs, such as those rising insurance premiums and property taxes.

The Credit Score Hurdle

Think of your credit score as the gatekeeper to your future front door. While you can often secure a loan with a score of 620, hitting that 740 mark is the “golden ticket” for snagging the most competitive interest rates. A higher score could save you hundreds of dollars every month, which adds up to tens of thousands over the life of your mortgage. If your score isn’t quite there yet, focus on paying down high-interest credit cards and avoiding any new debt for at least 90 days. You also need to keep a close eye on your debt-to-income ratio. Debt-to-income (DTI) ratio is the ratio of your monthly debt payments to your gross monthly income. Lenders use this figure to decide if you’re stretched too thin. While you’re crunching these numbers, understanding real estate basics can help you see how these financial figures impact your long-term equity and property value.

Saving for the Florida Lifestyle

Many first-time buyers assume the down payment is their only big upfront expense. In reality, you’ll need to budget for closing costs, which typically range from 2% to 5% of the home’s purchase price in Florida. It’s more than just the 3.5% down payment that you need to have ready. Based on current market data, a $400,000 home could require between $8,000 and $20,000 just for closing. You don’t want to be “house poor” the moment you move in. It’s wise to set aside an emergency repair fund from day one. Florida’s humidity and storm seasons can be tough on a property; having a cushion for a sudden AC repair or a roof issue provides immense peace of mind. If you’re thinking about how this purchase fits into your broader financial future, check out our landlord resources for tips on long-term planning and wealth building.

Finally, don’t settle for a generic pre-qualification. In a competitive market like Orlando or Lake Nona, you need a fully underwritten pre-approval letter. This tells sellers that a professional has actually verified your income and assets, making your offer much more attractive. Taking these proactive steps to buying a house in florida for the first time will give you the confidence to act fast when you find the perfect place.

Finding the Right Central Florida Neighborhood

Florida is famous for its “location, location, location” mantra, but in a high-growth state like ours, that phrase carries even more weight. You aren’t just buying a home; you’re investing in a neighborhood’s future trajectory. Choosing the right spot is one of the most exciting steps to buying a house in florida for the first time, yet it requires a careful balance. You have to weigh the proximity to Orlando’s job hubs against the local amenities that make a community feel like home. Online portals are helpful for browsing, but they often lead to listing fatigue. To avoid getting overwhelmed, it’s better to narrow your focus to a few key areas that align with your lifestyle and budget.

Spotlight on Central Florida Growth

Currently, Lake Nona and Winter Garden are booming for first-time buyers. Lake Nona is a hub for innovation and medical professionals, while Winter Garden offers a perfect mix of historic charm and modern retail. When you’re looking at these areas, always evaluate the school districts. Even if you don’t have kids, high-rated schools are a major driver of resale value. If those popular spots feel a bit out of reach, look toward Clermont or Apopka. These are the “hidden gems” of the 2026 market, offering more space and scenic views without the premium price tag of downtown Orlando. For a structured way to compare these communities, the University of Florida’s First-Time Homebuyer Guide provides excellent worksheets for assessing neighborhood quality.

Working with a Trusted Partner

Navigating these diverse pockets requires a partner who understands the street-level truth. It’s vital to know the difference between a listing agent and a buyer’s agent. A listing agent works for the seller, but a buyer’s agent is your dedicated advocate. At Morgan Property Solutions Inc., we pride ourselves on simplifying the search process. We help you look past the staging to see a home’s true potential and its fit within the community. You can read more real estate articles on our site to stay informed about local market trends. If you’re ready to start your journey with a steady ally, you can learn more about our team at Morgan Property Solutions Inc. and our commitment to your success. Taking these steps to buying a house in florida for the first time with expert guidance ensures you find a home that’s a perfect match for your future.

The “Florida Factor”: Insurance, Inspections, and Climate

Buying a home in the Sunshine State involves more than just picking out a floor plan or a backyard pool. You have to account for the “Florida Factor.” This includes the unique environmental and regulatory challenges that can make or break a deal. In fact, understanding these local nuances is one of the most vital steps to buying a house in florida for the first time. While you might be focused on the sales price, the ongoing costs of insurance and maintenance are what will truly define your monthly budget. In 2026, these factors are no longer secondary considerations; they are at the very heart of a successful purchase.

Navigating the Insurance Maze

Homeowners insurance has become a significant hurdle for many buyers. With average annual premiums in Florida now ranging between $5,500 and $11,000, you cannot afford to ignore this line item until the last minute. The age of the roof is often the most important number on a listing. Many carriers will outright refuse to cover a home if the roof is more than 15 years old, regardless of its actual condition. To secure a policy, you will likely need a 4-point inspection. A 4-point inspection covers the roof, electrical, plumbing, and HVAC systems. You should also ask for a wind mitigation report. This document proves your home has features like hurricane straps or impact-resistant windows, which can trigger substantial credits to lower your premiums. Without these credits, your monthly “all-in” payment could jump by hundreds of dollars.

The Inspection Period Strategy

A standard home inspection is a great start, but it isn’t enough in Florida. You need to be specific about what you’re looking for to avoid a “money pit.” We always recommend a separate Wood Destroying Organism (WDO) inspection. Termites are a reality here; catching an infestation early can save you from a structural nightmare. Additionally, pay close attention to flood zones. Even if you are miles from the coast, Central Florida’s heavy summer rains can cause localized flooding. Check the FEMA maps carefully before you sign. Use your inspection reports as a strategic negotiation tool. If the 4-point inspection reveals an aging electrical panel or a leaky pipe, you can ask the seller to fix these issues or provide a credit at closing. If the problems are too extensive or the seller won’t budge, don’t be afraid to walk away. Protecting your investment means knowing when a house will cost more than it’s worth. Mastering these steps to buying a house in florida for the first time ensures you aren’t just buying a house, but a safe and sustainable home.

From Offer to Closing: Crossing the Finish Line

You have navigated the neighborhoods and survived the inspections. Now, it’s time to put pen to paper. Crafting a competitive offer is one of the most high-stakes steps to buying a house in florida for the first time. It’s not just about the number on the page. It’s about showing the seller you’re a reliable partner who can actually cross the finish line. In a market that still moves quickly, your strategy at this stage determines whether you get the keys or go back to the drawing board.

The Art of the Offer

In fast-moving markets like Orlando, escalation clauses have become a popular tool. These allow your offer to automatically increase if a higher bid comes in, up to a limit you set. You also need to consider your “Earnest Money” deposit. This cash sits in an escrow account, which is a neutral third-party holding area that protects your money while the legal details are finalized. A clean offer, one with clear timelines and reasonable contingencies, often beats out a slightly higher price that feels “messy” or risky to a seller. If you want to ensure your offer stands out for the right reasons, professional Real Estate Buyer Representation can make all the difference in your negotiations.

Sometimes, the bank’s appraiser decides the home is worth less than your agreed-upon price. This is known as an appraisal gap. If this happens, you’ll need to negotiate with the seller to lower the price, cover the difference with your own cash, or use your appraisal contingency to walk away. It’s a common hurdle in 2026, but it doesn’t have to be a deal-breaker if you have a plan in place.

Final Steps and Funding

The most beautiful words you’ll hear during this process are “Clear to Close.” This means your lender has finished their final review and the money is ready to move. Before you head to the title company, you’ll perform a final walkthrough. This is your last chance to make sure the previous owners didn’t take the appliances or leave a giant hole in the wall. Check that the AC still works and run the faucets one last time to ensure everything is exactly as it should be.

On closing day, bring your photo ID and prepare for a workout. You’ll be signing a thick stack of documents that officially transfer ownership to you. Prepare your hand for a lot of signatures; it’s a lot of paperwork, but it’s the final barrier between you and your new home. Once the lender funds the loan and the deed is recorded, those keys are finally yours. It’s a methodical process, but seeing your name on that deed makes every bit of the effort worth it.

Life After Closing: Protecting Your Investment

Congratulations, you are officially a homeowner. While the heavy lifting of the purchase is over, the final steps to buying a house in florida for the first time involve protecting your new asset. In Florida, this starts with understanding your tax benefits and keeping up with the unique demands of our climate. You have worked hard to get here. Now it is time to make sure your investment works just as hard for you. Being proactive in the first few months will save you a lot of stress and money down the road.

Maximizing Tax Benefits

Your first major win after moving in is filing for the Florida Homestead Exemption. This is not an automatic process; you must apply through your county property appraiser’s office. This exemption can knock up to $50,000 off the assessed value of your primary residence, which leads to significant savings on your property taxes every year. You cannot afford to miss the March 1st deadline to file. If you miss that date, you’ll have to wait another full year to see those savings on your bill. Once you are homesteaded, you also gain the protection of a special assessment limit. The Save Our Homes amendment is a cap on annual assessment increases at 3% or the CPI. This ensures that even if home values in Orlando skyrocket, your tax bill stays predictable and manageable.

Maintaining the “Florida Lifestyle”

Maintenance in Florida looks a bit different than in other states. Your AC system is your home’s heartbeat. You should have it serviced at least twice a year to prevent costly failures during the July heat. If your new home has a pool, stay on top of the chemistry and filtration every single week. Neglecting a pool for even a short time can lead to an expensive “green swamp” situation that is difficult to fix. By staying ahead of these chores, you avoid the high-cost repairs that can drain your savings. It’s all about small, consistent efforts to keep the property in top shape.

Your Long-Term Real Estate Ally

Many of our clients find that their first home is just the beginning of their real estate journey. As you build equity, you might eventually consider turning this property into a rental while you move into something larger. This is where having a seasoned partner makes a huge difference. At Morgan Property Solutions, we help you transition from a first-time buyer to a savvy investor. You can Learn about us and our 20+ years of Central Florida experience to see how we support owners through every phase of property ownership. We’re here to help you manage your investment so you can focus on enjoying your new life in the Sunshine State. Taking these final steps to buying a house in florida for the first time sets you up for a lifetime of financial growth and security.

Ready to Make Your Florida Dream a Reality?

Owning a home in the Sunshine State is a rewarding journey, but it requires a careful approach. We have covered how to get your finances in order and why navigating the “Florida Factor” of insurance and inspections is so critical. Mastering the steps to buying a house in florida for the first time is about more than just finding a pretty kitchen; it is about building a secure financial future. From filing your Homestead Exemption to managing your long-term maintenance, every detail matters.

You don’t have to navigate this complex market alone. With over 20 years of Central Florida expertise and A+ rated professional guidance, our team is here to act as your steady ally. We specialize in the Orlando, Lake Nona, and Winter Park markets, ensuring you have the local insight needed to make a confident decision. Whether you are looking for your first starter home or a long-term investment, we are committed to your success.

Start your Central Florida home search with Morgan Property Solutions today. We look forward to helping you find the perfect place to call home.

Frequently Asked Questions

Is there a first-time homebuyer program specifically for Florida?

Yes, Florida offers several impactful programs like the Hometown Heroes Program, which provides up to $35,000 in assistance for eligible professionals. Other options include Florida Assist, offering up to $10,000 as a 0% interest deferred second mortgage, and the Florida Homeownership Loan Program (FL HLP). These initiatives are specifically designed to help you manage the upfront costs of a down payment and closing fees.

How much money do I need to save for a down payment in Florida?

The amount depends on your loan type, but many first-time buyers use FHA loans which require a 3.5% down payment. For a Florida home at the median price of $425,000, that equals $14,875. Some conventional programs allow for as little as 3% down. It’s vital to remember that you’ll also need separate funds for closing costs and an emergency repair cushion.

What is the average closing cost for a house in Orlando?

In Orlando, you should budget between 2% and 5% of the purchase price for closing costs. If you’re buying a home at the metro median of $385,000, your closing costs will likely range from $7,700 to $19,250. This total includes Florida’s specific taxes, such as the documentary stamp tax on mortgages and the intangible tax, along with title insurance and loan origination fees.

Can I buy a house in Florida with a 600 credit score?

Yes, you can qualify for a mortgage with a 600 credit score, particularly through FHA or VA loan programs. While a 580 is often the minimum for FHA, a score of 600 gives you more lender options. However, keep in mind that improving your score before starting the steps to buying a house in florida for the first time will help you secure a much lower interest rate.

What is the Homestead Exemption and how do I apply?

The Homestead Exemption is a legal provision that reduces the taxable value of your primary residence by up to $50,000. You apply through your local county property appraiser’s office after you’ve made the home your permanent residence. You must own the home by January 1st and submit your application by the March 1st deadline to receive the benefit for that tax year.

How long does the home buying process take from start to finish?

The entire journey typically takes three to six months, depending on how quickly you find a property. Once you have a signed contract, the closing process usually takes 30 to 45 days for financing and inspections. Current market data shows that homes in Central Florida stay on the market for an average of 77 days, so patience is a key part of the strategy.

Do I need a lawyer to buy a house in Florida?

Florida does not legally require you to hire an attorney to complete a residential real estate transaction. Most buyers work with a real estate agent and a title company to handle the contracts and the closing process. However, if you’re dealing with a complex legal situation or a unique property dispute, you might choose to hire a lawyer for an extra layer of protection.

What is a 4-point inspection and why is it required?

A 4-point inspection is a focused review of a home’s roof, electrical, plumbing, and HVAC systems. Most insurance companies in Florida require this report for any home older than 15 years before they will issue a policy. It is one of the most critical steps to buying a house in florida for the first time because it proves the home’s major systems are safe and insurable.

Article by

Oliver Overton-Morgan

Oliver Overton-Morgan is a full-time Real Estate Broker since 2003, with years of experience helping thousands of people purchase and sell real estate throughout Central Florida. He holds a Graduate Realtor Institute designation, LCAM, and has held licenses in good standing as a Florida Mortgage Broker and a Notary Public. Oliver immigrated to central Florida in 2001, and within 5 years Oliver built a successful Real Estate brokerage in central Florida, where he recruited over 75 Sales Associates with 25+ million in sales production.